Key Takeaways

- More than half of asset managers already use or plan to deploy AI for advisor segmentation within the next 12 months, according to Cerulli Associates research.

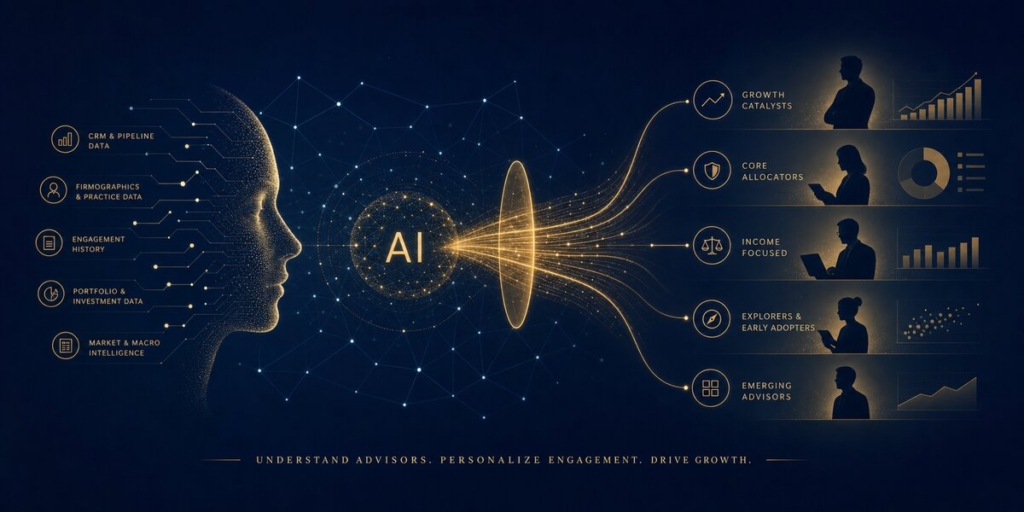

- Effective AI segmentation combines four data layers — FINRA holdings, third-party aggregators, custodian feeds, and first-party CRM signals — to score advisors on product affinity and engagement recency.

- AI coverage workflows automate the sequence of touchpoints after a tier is assigned: personalized email, content delivery, and wholesaler alert triggers.

- The leading AI architecture for fund distribution uses a dedicated Advisor Intelligence Agent that monitors data feeds continuously, re-scores advisor lists, and passes prioritized queues to outreach agents.

- Fund issuers that redesign distribution around AI-native workflows stand to capture 25 to 40 percent of their total cost base in efficiency gains, per McKinsey analysis.

Advisor segmentation has always been a core function of fund distribution. The challenge has never been the theory — divide advisors into tiers based on AUM, channel, product affinity, and responsiveness, then direct resources accordingly. The challenge has been execution at scale. Coverage teams are finite. Advisor universes are large. Data is fragmented across custodians, broker-dealers, and third-party providers. The result, for most fund issuers, is a segmentation model that lives in a spreadsheet, ages quickly, and never fully drives daily sales activity.

AI changes the execution problem. When a purpose-built Advisor Intelligence Agent monitors data feeds continuously, scores advisors against a dynamic model, and routes prioritized queues directly to wholesalers and automated outreach sequences, segmentation stops being a quarterly planning exercise and becomes a live operational system. This article covers the models, data sources, and workflows fund issuers need to build that system in 2026.

Lead-Lag Media® is an AI-driven sales, marketing, and distribution firm for the financial services industry. More than 80 AI agents work for our clients around the clock. The conversations that move money still happen between people. AI does the work. Humans make the connections. Our work with fund issuers on segmentation workflows informed much of what follows.

Why Traditional Advisor Segmentation Breaks Down

The standard segmentation approach segments advisors into three or four tiers based on production or AUM thresholds. Tier one advisors receive proactive wholesaler coverage. Tier two advisors receive periodic calls and digital outreach. Tier three and below receive little to no direct attention. This model has a structural problem: the inputs are static and the outputs are manual.

Advisors change. An advisor who appears in tier three this year based on last year’s data may have grown their practice significantly, taken on a new asset allocation mandate, or shifted platforms entirely. Without continuous monitoring, the issuer misses the signal. Meanwhile, their competitor — who happens to have a better data refresh cycle — captures the relationship first.

The second problem is data fragmentation. Advisor data lives in multiple incompatible systems: CRM, broker-dealer records, custodian feeds, conference attendance, email engagement metrics, and third-party intelligence platforms. Without an integrating layer, no human analyst can synthesize these sources into a real-time scoring model for a universe of 10,000 or more advisors. The spreadsheet cannot keep up.

The third problem is coverage capacity. The wholesaler-to-advisor ratio at most firms means that even a well-designed static tier model will leave large portions of the addressable market without meaningful contact. A Cerulli Associates report on U.S. Intermediary Distribution 2025 underscores that granular advisor segmentation, combined with technology tools, represents one of the primary growth levers available to asset managers seeking to maximize product distribution through intermediaries.

The Four Data Layers for AI Advisor Segmentation

An AI segmentation model is only as good as its inputs. Fund issuers who attempt to build scoring systems on single-source data — typically a CRM export or a single broker-dealer report — get models that score confidently but predict poorly. The architecture that works combines four distinct data layers.

Layer One: Regulatory and Holdings Data

FINRA BrokerCheck and Form ADV filings provide baseline advisor registration data: firm affiliation, registration type, years of experience, disciplinary history, and primary office location. This layer is free, structured, and authoritative. It also identifies channel classification — wirehouse, independent broker-dealer, hybrid RIA, fee-only RIA — which is the most fundamental segmentation variable for fund distribution because different channels have different product approval gates, fee structures, and client demographics.

Third-party holdings aggregators such as Broadridge DST add the next critical layer: which advisors are currently allocating to which products and in what volume. This transforms segmentation from a demographic exercise into a behavioral one. An advisor holding a competing large-cap active ETF from a different issuer is a higher-probability prospect for a comparable product than an advisor who has never allocated to the category.

Layer Two: Practice and AUM Intelligence

The second layer captures practice growth signals. Wealth intelligence platforms compile data on advisor AUM, client counts, platform moves, team hires, and firm transitions. An advisor who has grown AUM by 20 percent over the past 12 months represents a different distribution opportunity than one with a flat book — regardless of their current tier assignment based on static thresholds.

According to Cerulli’s U.S. Advisor Metrics 2025, team-based advisor practices deliver annual organic growth of more than $20 million on average, compared with $8 million for solo practices. Identifying advisors moving toward team structures — a leading indicator of accelerating growth — is a high-value signal that only systematic data aggregation can capture at scale.

Layer Three: Engagement and Intent Signals

The third layer is first-party engagement data: email open rates, content download history, webinar attendance, website visit patterns, and conference interactions. These signals measure current attention, not historical behavior. An advisor who has opened three product emails in the past 30 days but has not yet allocated is a higher-priority outreach target than one who allocated two years ago and has not engaged since.

Most fund issuers have this data sitting unused in email platforms and CRM systems. The gap is integration: connecting engagement signals to the segmentation model so that the AI can continuously update scores based on real-time intent rather than waiting for a quarterly data refresh.

Layer Four: Market and Positioning Context

The fourth layer adds context that explains why advisor behavior is shifting. This includes rate environment data, equity market performance, regulatory changes affecting product structures, and competitor product launches. An AI agent that incorporates context can explain why a particular advisor’s score changed — not just that it did — and can proactively alert wholesalers to emerging opportunities before they show up in transaction data.

The AI Segmentation Model Architecture

With the four data layers in place, the segmentation model itself can be structured around a composite scoring engine. The engine assigns each advisor a score across five dimensions: product-category affinity, practice growth trajectory, channel alignment, engagement recency, and competitive displacement opportunity. Each dimension is weighted based on the issuer’s current product lineup and distribution priorities.

The output is not a static tier label but a dynamic rank-ordered list that the AI updates continuously as new data arrives. This matters operationally. A wholesaler logging into their dashboard on Monday morning sees a list of advisors sorted by current opportunity score, not by last quarter’s tier assignment. The highest-probability conversations are always at the top.

The Advisor Intelligence Agent — the specific AI workflow architecture Lead-Lag Media deploys for issuer clients — operates as an always-on monitoring and scoring system. It pulls from the four data layers on configurable refresh cycles (some signals update daily, others weekly), recalculates scores, flags material changes, and automatically routes updated queues to the relevant outreach agents or wholesaler CRM records. No human analyst has to rebuild the model or re-sort the list. The agent does it.

According to the 2025 MMI-Broadridge Annual Survey, 61 percent of asset and wealth management firms expect AI to be a high strategic priority moving forward — more than double the 38 percent who said the same the prior year. The shift from exploration to implementation is underway across the industry, and distribution is one of the highest-ROI applications.

Coverage Workflow Design: From Score to Action

Segmentation without workflow automation produces lists that no one acts on. The second component of an effective AI distribution system is a structured coverage workflow that triggers specific actions based on tier assignment and score changes.

A basic three-tier coverage workflow operates as follows. Tier one advisors — those above a composite score threshold indicating high product affinity and strong growth trajectory — trigger immediate wholesaler alert and a personalized outreach sequence. The AI generates a wholesaler briefing document: advisor background, current holdings, recent engagement, and suggested talking points tailored to the advisor’s channel and practice profile. The outreach sequence begins in parallel: a customized email with relevant product content, followed by a calendar invite from the wholesaler if the first email generates a click.

Tier two advisors enter a sustained nurture sequence. The AI delivers content calibrated to their inferred interests — based on the products they currently hold, the channels where they operate, and the market context relevant to their practice — on a regular cadence. When an engagement signal pushes their score above the tier one threshold, the AI automatically escalates them to the wholesaler queue.

Tier three advisors receive lighter-touch digital outreach at a lower frequency. The AI still monitors their signals continuously; a material score change at any time can promote them to a higher tier and trigger the corresponding action sequence without human review.

The Broadridge 2026 Advisor Survey found that 51 percent of advisors now use generative AI across at least one area of their business, and that client engagement and marketing are the top reported benefits. Advisors are changing how they consume information and how they expect to be contacted. AI-powered outreach that delivers personalized, relevant content at the right moment is increasingly aligned with how advisors actually want to work with product partners.

Data Infrastructure Requirements

The practical question for most fund issuers is not whether AI segmentation works — the evidence base is clear — but how to build the data infrastructure that makes it operational. Three infrastructure components are non-negotiable.

The first is a unified data environment. Advisor data from disparate sources must be normalized into a single record per advisor before scoring can happen reliably. This means establishing a common advisor identifier (typically CRD number from FINRA), mapping all data sources to that identifier, and maintaining deduplication logic as new data arrives. Without a unified record, the AI will score fragments of an advisor’s profile, not the full picture.

The second is API connectivity for real-time data feeds. The highest-value segmentation signals — email engagement, website visits, content downloads — are only actionable if they flow into the scoring model in near-real time. A daily batch feed degrades the signal. Configuring webhook or API connections between the marketing platform, CRM, and scoring engine is a technical investment that pays back quickly in coverage team efficiency.

The third is governance and compliance logging. Fund distribution operates in a regulated environment. Every AI-generated communication, every automated outreach sequence, and every wholesaler alert triggered by the system needs to be logged and auditable. The infrastructure design must build this logging in from the start, not retrofit it after deployment.

Metrics That Prove the Model Is Working

Fund issuers need to measure the performance of their AI segmentation system against distribution outcomes, not just process efficiency. The metrics that matter most are: advisor conversion rate by tier (what percentage of tier-one advisors allocate within 90 days of entering the tier), average time-to-first-allocation for advisors who entered through the AI system versus prior manual coverage, and score accuracy (how often does a high composite score predict a subsequent allocation).

Secondary metrics include wholesaler productivity — calls completed per day, pipeline value generated per region — and content engagement rates by segment. If tier-one advisors are not opening the personalized emails the AI generates, the content model needs recalibration. If tier-two advisors are converting at higher rates than tier-one, the scoring model weights need adjustment.

The AI system should surface these metrics automatically. The Advisor Intelligence Agent tracks outcome data alongside scoring data and runs regular feedback loops: which advisor attributes predicted allocation, which content assets drove clicks, which wholesaler briefings led to calls. These feedback loops allow the model to improve continuously rather than remaining static.

For fund issuers building toward full AI-native distribution, the long-term metric is coverage ratio: what percentage of the addressable advisor universe receives meaningful, data-informed contact at appropriate intervals. With human-only coverage teams, this number is typically under 20 percent for most issuers. With AI-automated outreach sequences handling tiers two and three, coverage ratios above 80 percent become operationally achievable. That gap — the advisors who currently receive no contact from your firm — is where distribution growth lives.

To learn more about how fund issuers are deploying AI agents for distribution, visit our issuers overview or explore what AI-native workflows look like in practice on our how it works page. If you manage an advisor practice and want to understand how these tools apply to your business, see our advisor resources.

Related Reading

- AI Agents for Fund Issuers in 2026: What General-Purpose AI Launches Do Not Solve for Distribution

- Agentic AI for Asset Management: A Distribution Playbook for Fund Issuers (2026)

- Marketing Automation for Fund Issuers (2026)

Frequently Asked Questions

What data sources power AI advisor segmentation for fund issuers?

The most effective AI segmentation models draw from four data layers: broker-dealer reported holdings via FINRA, third-party data aggregators such as Broadridge DST, custodian transaction feeds, and first-party CRM signals. Combining these layers lets an AI engine score each advisor on product affinity, AUM tier, channel type, and engagement recency without relying on a single incomplete dataset.

How do fund issuers prioritize which advisors receive outreach from an AI workflow?

Prioritization models rank advisors on a composite score that weights current product holdings, historical responsiveness to similar strategies, practice AUM growth trajectory, and channel alignment. Advisors who already hold comparable products from competing issuers score higher than cold contacts because they have demonstrated product-category acceptance. AI re-scores the list on a rolling basis as new data arrives, so coverage teams always work the highest-probability targets first.

What is the difference between a segmentation model and a coverage workflow in AI distribution?

A segmentation model classifies advisors into tiers based on data-derived scores. A coverage workflow is the automated sequence of actions the AI takes once an advisor enters a tier: personalized email at day one, product PDF at day three, wholesaler alert at day seven, and so on. Segmentation tells you who to reach. The workflow tells the AI agents what to do, when, and through which channel.

Can small fund issuers with limited data budgets use AI segmentation?

Yes. The entry point is not a massive proprietary data infrastructure. Smaller issuers can start with a curated advisor list from public FINRA data, layer on a single third-party enrichment feed, and run a lightweight scoring model inside a CRM such as HubSpot or Salesforce. The goal is structured, repeatable prioritization, not perfection. AI agents then execute outreach sequences on the prioritized list, generating first-party engagement data that improves segmentation over time.

About the Author: Michael A. Gayed, CFA, is the founder of Lead-Lag Media® — an AI-driven sales, marketing, and distribution firm for the financial services industry — and publisher of The Lead-Lag Report on Substack.